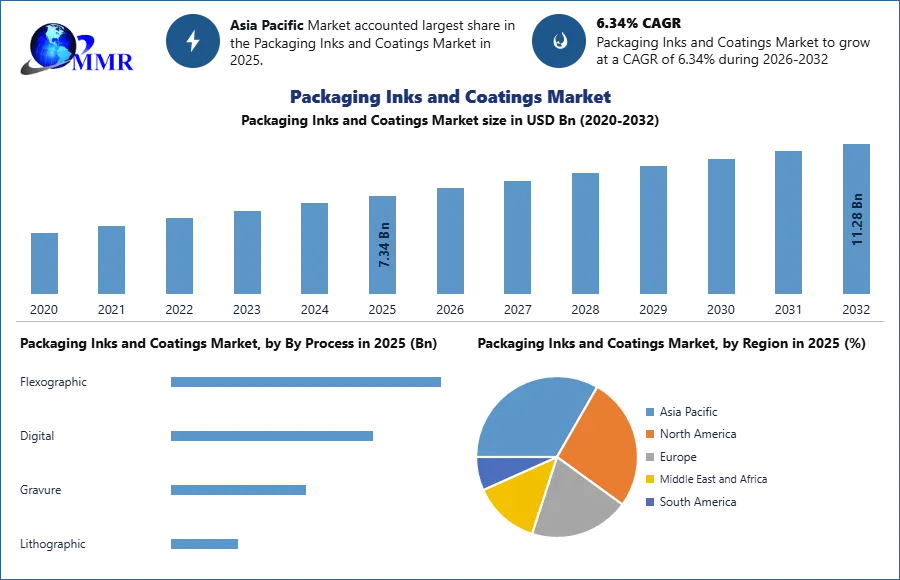

Global Packaging Inks and Coatings Market Accelerates with Innovations in Digital Printing and Smart Packaging

Literature |

2026-06-22 14:29:58

Mise à niveau vers Pro

The global Software Defined Data Center Market Size has expanded into a formidable, multi-billion-dollar industry, reflecting its status as a cornerstone of modern digital transformation strategies. Current valuations place the market in the tens of billions of dollars, but the truly compelling story is its growth trajectory. Analysts consistently forecast a powerful compound annual growth rate (CAGR), often in the range of 20% to 30%, which will propel the market to be worth well over a hundred billion dollars within the next five to seven years. This impressive scale and rapid expansion are not merely driven by routine IT refresh cycles; they are a testament to a fundamental architectural shift. The market size represents the total global investment in the software, services, and integrated systems required to transform rigid, legacy data centers into agile, cloud-like environments. As enterprises increasingly recognize that agility and automation are critical for survival and growth, the investment in the foundational SDDC technologies that enable these capabilities continues to surge, solidifying the market's substantial valuation and its bright future outlook.

Deconstructing the market size by its core technological components reveals the different maturity levels and growth dynamics within the industry. The Software-Defined Compute (SDC) segment, essentially server virtualization, accounts for a large and mature portion of the market, forming the foundational layer upon which everything else is built. While its growth rate is more moderate, it remains the largest single component. The Software-Defined Storage (SDS) segment is a high-growth area, as organizations are aggressively moving away from expensive, proprietary SANs towards more flexible and cost-effective, software-based storage solutions that run on commodity hardware. The fastest-growing component, however, is often Software-Defined Networking (SDN). As enterprises seek to achieve true automation and implement advanced security models like micro-segmentation, the adoption of SDN is accelerating rapidly. Finally, the overarching management and automation software layer is a significant and increasingly valuable part of the market, as it is the "brain" that unifies all the components and delivers the promised agility and operational efficiency.

When analyzed by end-user industry, the market size is broadly distributed, highlighting the universal appeal of the SDDC model. The Banking, Financial Services, and Insurance (BFSI) sector is one of the largest consumers, driven by an intense need for security, regulatory compliance, operational resilience, and the agility to compete with nimble fintech startups. The IT and Telecommunications sector is another massive contributor, as service providers and cloud companies use SDDC principles to build the very public and private cloud services they sell to their own customers. Other major verticals include healthcare, which requires a secure and agile infrastructure to handle sensitive patient data and power digital health initiatives; retail, particularly for supporting the massive scalability demands of e-commerce platforms; and government agencies, which are under mandates to modernize their IT infrastructure and improve efficiency. This diverse industry adoption provides a stable and resilient foundation for the market's continued growth.

From a regional perspective, North America currently holds the largest share of the global SDDC market size. This dominance is due to the region's early adoption of virtualization technologies, the heavy concentration of major technology vendors and cloud hyperscalers, and significant IT spending by its large enterprise sector. Europe follows as a substantial and mature market, with strong growth often driven by data sovereignty regulations like GDPR, which encourage the building of robust, in-country private clouds. The most dynamic growth story, however, is in the Asia-Pacific (APAC) region. Propelled by rapid economic development, massive government-backed digitalization projects, and the construction of new, state-of-the-art data centers in countries like China, India, and Singapore, APAC is projected to exhibit the highest CAGR over the forecast period. This will make it the central arena for competition and expansion as vendors vie to capture a share of the world's fastest-growing digital economies.

Explore Our Latest Trending Reports:

Prison Management System Market

Process Analytical Instrumentation Market