Chemical Characterization: Building Confidence in Scientific Results

Other |

2026-07-06 14:00:11

ترقية الحساب

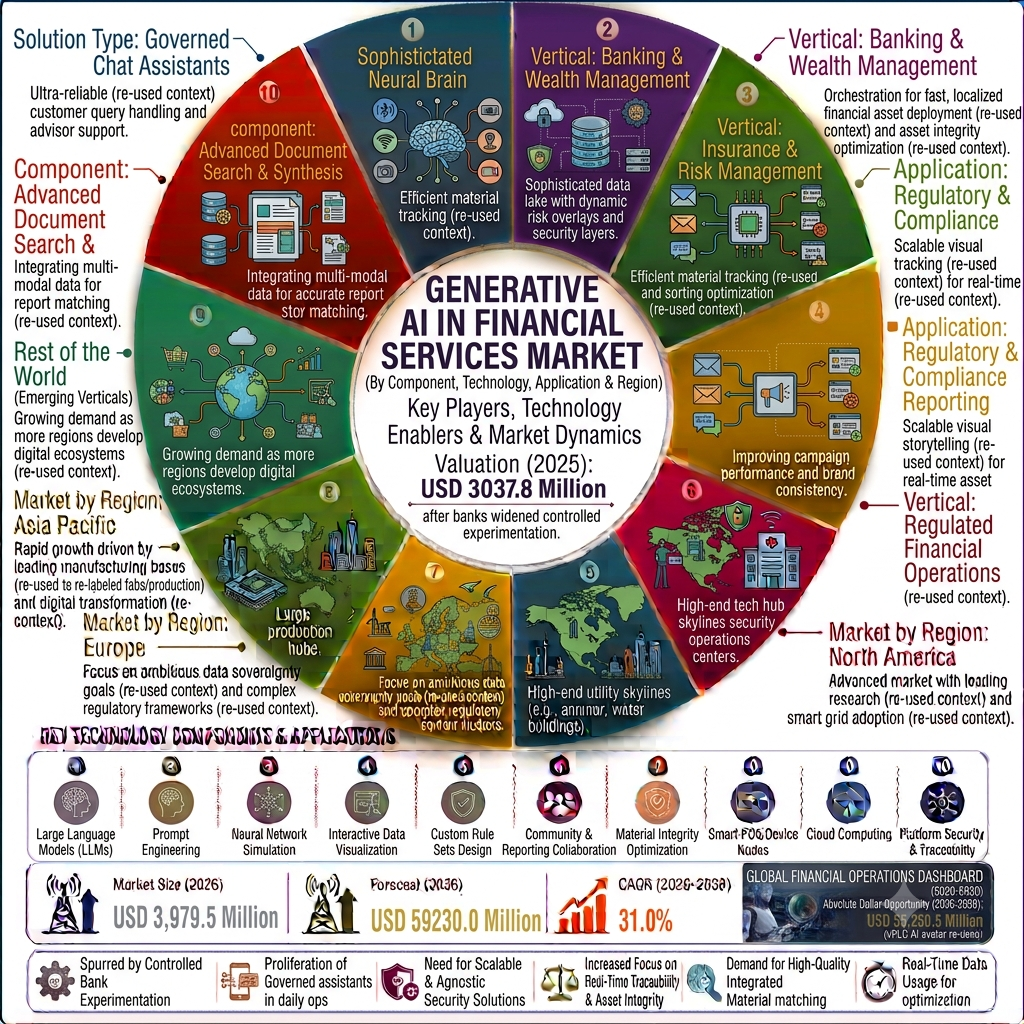

According to a comprehensive industry study published by Fact.MR, the generative AI in financial services market crossed an initial sector valuation of USD 3037.8 million in 2025.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.factmr.com/connectus/sample?flag=S&rep_id=15539

Driven by an intensifying requirement to automate complex documentation, modernize fraud detection systems, and scale personalized customer engagement, the global market is estimated to reach USD 3,979.5 million in 2026. Looking toward the conclusion of the ten-year forecast timeline, the industry is projected to reach an absolute market valuation of USD 59230.0 million by 2036. This trajectory represents a robust compound annual growth rate (CAGR) of 31.0% from 2026 to 2036, creating a significant multi-billion dollar opportunity for software developers, managed service providers, and financial systems integrators.

Key Market Highlights at a Glance

Why Is the Generative AI in Financial Services Market Growing?

"Generative AI has evolved from a creative tool into a core component of the financial services infrastructure," states a senior market analyst at Fact.MR. "Institutions are prioritizing software that provides orchestration and monitoring around models, as the focus shifts toward maintaining evidence-heavy control requirements in customer-facing and internal risk management workflows."

Component Breakdown: Software Leads the Infrastructure Investment

Software platforms represent the critical foundation for generative AI adoption within the financial sector. The software segment is expected to account for a 50.5% share of the overall market in 2026. This dominance is driven by the necessity for enterprise-grade orchestration layers and embedded copilots that integrate seamlessly with existing core-banking and financial reporting platforms. While services play a role in integration and policy design, the scalability of software subscriptions makes them the preferred vehicle for widespread organizational adoption.

Application Dynamics: Workflow Automation Drives Operational Efficiency

As financial organizations seek to optimize internal processes, workflow automation has emerged as the most critical application for generative AI. The workflow automation segment is estimated to hold a 47.1% market share in 2026. This is shaped by the prevalence of repeatable case management and documentation tasks that are highly suitable for supervised generation. By inserting AI into these steps, banks and insurers can maintain human-in-the-loop oversight while dramatically accelerating service delivery and administrative output.

Organization Size Insights: SMEs Drive Rapid Deployment

Small and Medium Enterprises (SMEs) are emerging as the primary engines of generative AI adoption, capturing a 48.3% market share in 2026. This trend is driven by the availability of packaged, cloud-based AI assistants that eliminate the need for large, internal model-engineering teams. While large enterprises focus on complex permission design and core-system integration, SMEs are leveraging these accessible tools to achieve rapid productivity gains and improve their competitive positioning against traditional incumbents.

Market Dynamics

Core Market Drivers

The primary driver of the global market is the strategic shift toward incorporating AI into regulated financial workflows. As regulatory bodies and internal risk functions formalize AI governance, the demand for platforms that provide transparency, auditability, and clear scope boundaries is accelerating. Furthermore, the rise of digital banking and the increasing prevalence of online financial fraud continue to drive investments in AI-powered forecasting and threat detection systems.

Primary Market Restraints

The main restraint limiting faster adoption is the implementation gap between initial pilot programs and full-scale business integration. Measuring the enterprise value and profitability of AI deployment remains difficult for many large institutions, leading to cautious procurement cycles. Additionally, data residency requirements and strict security controls regarding core financial systems can complicate the deployment of cloud-based generative AI tools.

Prominent Industry Trends

The most important trend reshaping the market is the rise of agentic AI, which is expected to be a major growth frontier by 2030. Financial institutions are increasingly adopting "guardian agent" technologies that provide runtime assurance and compliance monitoring for autonomous AI. This focus on "permission layers" for enterprise AI allows firms to gain the benefits of automation while mitigating the risks of scope drift or safety failures.

Regional Outlook: Asia-Pacific Poised for Rapid Growth

The strategic push toward digital finance infrastructure and innovation is creating distinct growth profiles across global markets.

Australia is anticipated to advance at a 30.8% CAGR over the assessment period. This growth is primarily attributable to licensee experimentation within an active and supportive regulatory governance review environment, which encourages both small and large firms to test AI use cases.

The United Kingdom is forecast to expand at a 30.5% CAGR between 2026 and 2036. This growth trajectory is underpinned by broad adoption across traditional banks and insurance firms, which are leveraging generative AI to meet strict regulatory reporting obligations while simultaneously enhancing their customer service delivery.

Competitive Landscape: Focus on Auditable AI and System Integration

The competitive landscape for generative AI in financial services is defined by a race to provide auditable, enterprise-ready AI solutions. Companies are moving away from general-purpose offerings to provide specialized orchestration platforms that prioritize security, traceability, and seamless integration with existing financial data stacks.

Competitive dynamics show that providing only the base AI model is no longer sufficient. Market leaders are those that offer the "control point" between experimentation and production, allowing financial officers to trust AI agents with customer data, financial reporting, and risk-sensitive decisions.

Read the Comprehensive Industry Report: https://www.factmr.com/report/generative-ai-in-financial-services-market

Frequently Asked Questions

What is the projected global value of the generative AI in financial services market by 2036?

The generative AI in financial services market is projected to reach an absolute valuation of USD 59.23 billion by the year 2036 as institutions move from controlled experimentation to full-scale operational governance.

What is the expected compound annual growth rate of the generative AI in financial services industry?

The generative AI in financial services industry is forecast to expand at a compound annual growth rate (CAGR) of 31.0% from 2026 to 2036 as banks and insurers integrate governed assistants into their daily operations.

Which component segment holds the largest share within the generative AI in financial services market?

The software segment holds the largest position in the marketplace, accounting for a 50.5% share in 2026 due to the increasing demand for orchestration and monitoring layers that support AI deployment.

What application segment leads the generative AI in financial services industry in implementation volume?

The workflow automation segment leads the application landscape, capturing a 47.1% share of the global market in 2026 as institutions incorporate generative AI into repeatable case management and document-handling steps.

Which organization size segment is the largest adopter of generative AI in financial services?

Small and Medium Enterprises (SMEs) are the largest adopters, capturing a 48.3% share of the market in 2026 because packaged cloud-based tools reduce the need for large internal AI engineering teams.

What deployment environment leads the generative AI in financial services industry?

Cloud architectures lead the implementation landscape, capturing a 43.8% share of the global market in 2026 due to the benefits of managed model access and elastic inference capacity.

To View Related Report:

Generative Design Market: https://www.factmr.com/report/generative-design-market

Generative CNC Market: https://www.factmr.com/report/generative-cnc-market

Generative Design Software Market: https://www.factmr.com/report/3437/generative-design-software-market

Generative Design Tools for Recyclable Packaging Market: https://www.factmr.com/report/generative-design-tools-for-recyclable-packaging-market