Macchina Marcatrice Laser: Soluzioni Professionali per Marcature di Alta Precisione e Produzione Moderna

Other |

2026-08-06 06:03:09

Atualize para o Pro

Many buyers focus only on interest rates. But the truth is that the type of mortgage loan you choose can impact your monthly payments, flexibility, tax benefits, and overall financial comfort for years.

This guide breaks down mortgage loans in India in a simple way, helping you understand your options before signing any loan agreement.

A mortgage loan is a secured loan where the borrower pledges property as collateral to obtain financing from a bank or housing finance company. If repayments are not made according to the agreement, the lender has the legal right to recover dues through the mortgaged property.

In India, mortgage loans are commonly used for purchasing homes, constructing houses, buying commercial spaces, or raising funds against existing property.

Imagine Rahul, a young software engineer in Gurgaon. He wanted to buy a ₹70 lakh apartment but had savings of only ₹15 lakh. A home loan allowed him to purchase the property while paying manageable monthly installments over 20 years.

This is exactly how mortgage financing helps millions of Indian families become homeowners.

Interest rates directly affect your monthly EMI and total repayment amount.

A fixed-rate mortgage keeps the interest rate unchanged throughout the agreed period.

Best For:

Benefits:

Example:

If your EMI is ₹35,000 today, it remains largely unchanged even if market interest rates increase.

The interest rate changes according to market conditions and lender benchmarks.

Best For:

Benefits:

A hybrid mortgage combines fixed and floating rates.

Typically, the interest remains fixed for the first few years and then shifts to a floating structure.

Benefits:

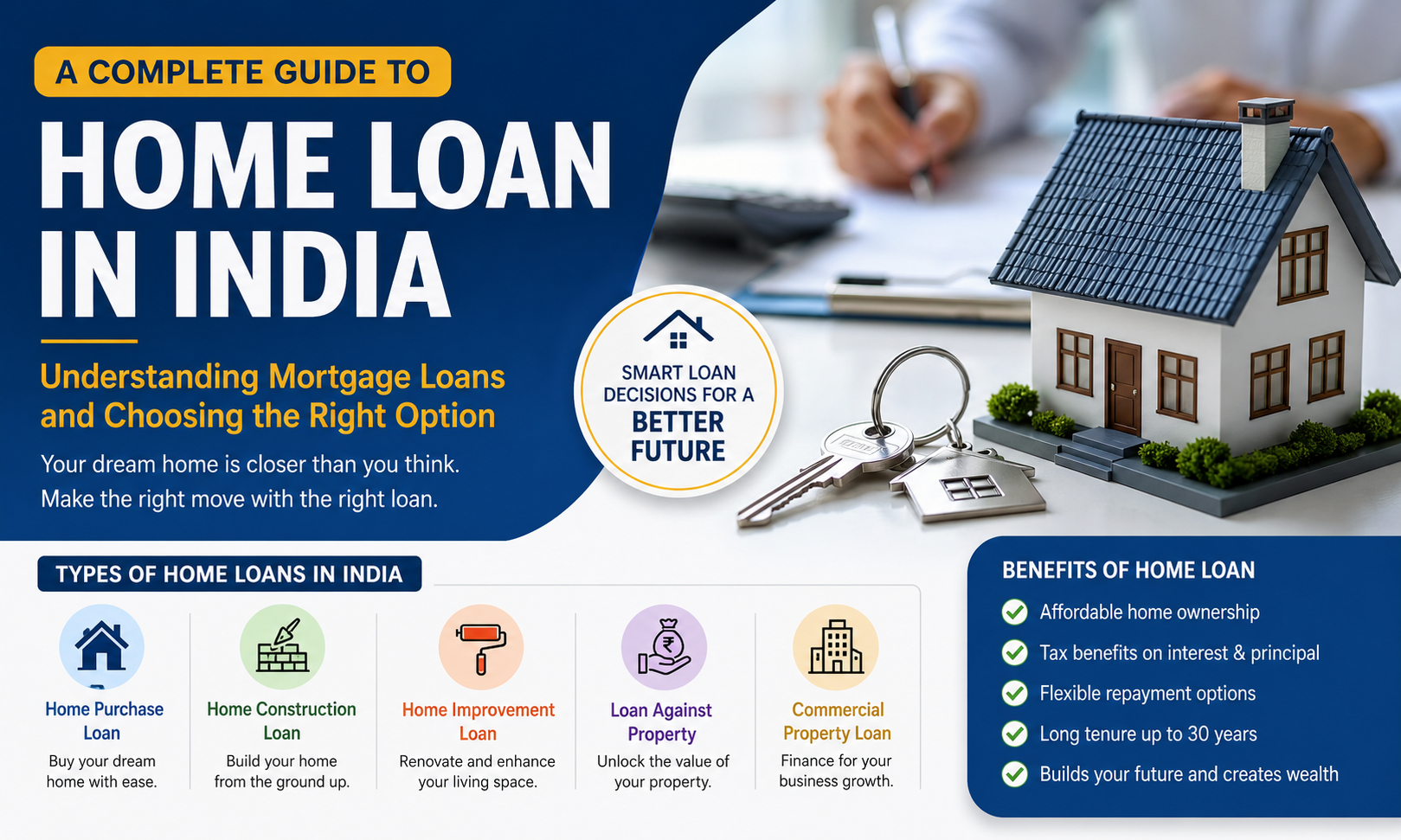

Different borrowing goals require different loan structures.

Used to buy a ready-to-move-in or under-construction residential property.

Designed for people building a house on their own land.

Used for renovations, repairs, or modernization projects.

Suitable for adding extra rooms, floors, or expanding existing structures.

Borrowers mortgage an existing property to raise funds for business, education, medical expenses, or other financial needs.

Example:

A business owner may mortgage a commercial property to secure working capital instead of taking a high-interest unsecured loan.

The intended use of the property often determines the mortgage category.

Used for homes, apartments, villas, and residential plots.

Used for offices, retail stores, warehouses, and commercial buildings.

Designed for factories, manufacturing units, and industrial infrastructure.

Available against agricultural land and farming-related assets, subject to local regulations and lender policies.

Indian property law recognizes several mortgage structures.

The borrower commits to repayment while the property remains as security.

Often called an equitable mortgage, it involves depositing original property documents with the lender.

The lender receives income generated by the property until the debt is repaid.

Ownership is conditionally transferred to the lender until repayment obligations are fulfilled.

The property sale becomes permanent if repayment conditions are not met.

A customized mortgage arrangement that combines features of multiple mortgage types.

Interest rates vary depending on lender policies, borrower profiles, credit scores, and loan tenure.

Generally:

Before choosing a lender, compare:

Choosing the right mortgage offers more than just financing.

Instead of waiting years to save the entire property value, buyers can purchase immediately.

Eligible borrowers may claim deductions on principal repayment and interest payments under applicable tax provisions.

Tenures often extend up to 30 years, reducing EMI pressure.

Property values may appreciate over time, helping build long-term wealth.

Various loan structures cater to different income levels and financial goals.

Let's consider a practical scenario.

Priya plans to buy a ₹80 lakh apartment.

The bank evaluates her:

After approval, funds are released to the seller. Priya repays the loan through monthly EMIs until the entire amount is cleared.

Once repayment is complete, the lender removes its claim on the property and full ownership remains with Priya.

Calculate affordability before property hunting.

Lenders review:

Evaluate loan terms, rates, fees, and service quality.

Common documents include:

The lender verifies legal ownership and property value.

The bank issues a sanction letter outlining loan terms.

Funds are released based on the property transaction stage.

Monthly installments continue until the loan is fully repaid.

Hidden charges can increase the total borrowing cost.

A stronger credit profile often leads to better loan offers.

Keep EMI commitments manageable within your monthly income.

Even small rate differences can result in significant long-term savings.

Home purchase loans with floating interest rates are among the most widely used mortgage options.

Fixed-rate or hybrid mortgages often suit first-time buyers who prefer payment stability.

Many lenders allow partial or full prepayment, though terms vary.

A higher credit score improves approval chances and may help secure better rates.

Yes. A home loan is specifically for purchasing or constructing property, while a loan against property uses an existing property as collateral to raise funds.

Finding the right mortgage isn't about selecting the lowest interest rate alone. It's about matching the loan structure with your financial goals, income stability, and future plans.

Whether you're exploring home loan types in India for your first property or comparing mortgage loans in India for investment purposes, understanding each option helps you make informed decisions. A carefully chosen mortgage can make homeownership smoother, more affordable, and financially rewarding for years to come.